Inflight Connectivity Report: Bridging the Gap Between IFC Expectations and Reality

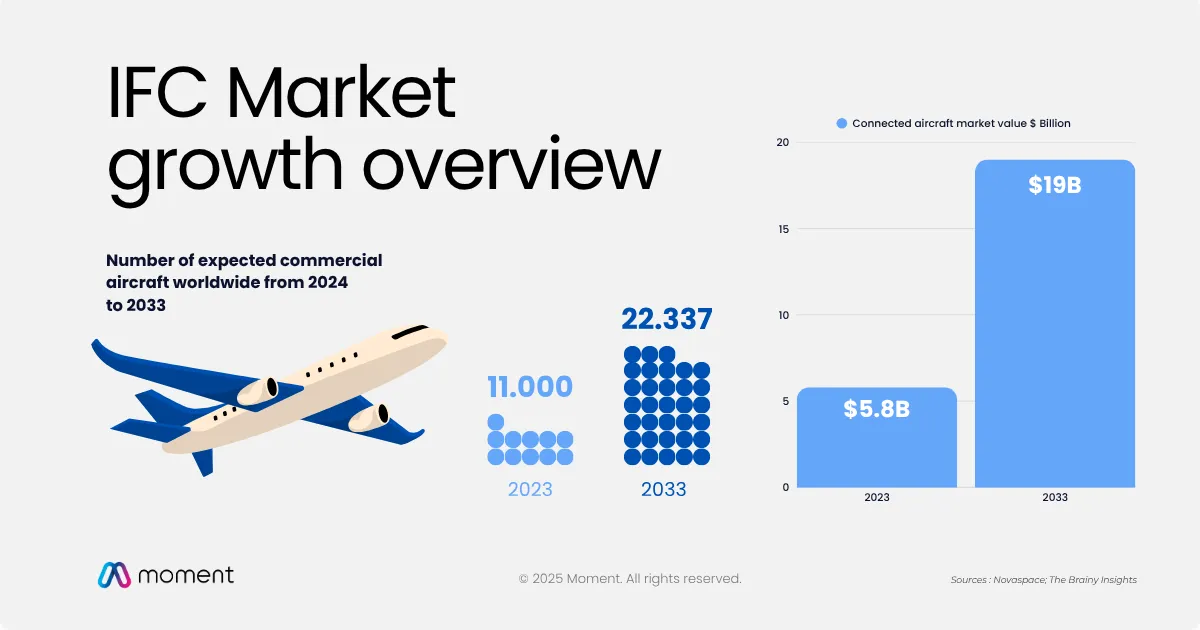

The inflight connectivity market is projected to reach $19B by 2033. This report covers the real costs, bandwidth requirements and connectivity architecture decisions airlines need to make, and where satellite-only approaches fall short.

Key findings

- A wide-body long-haul flight requires approximately 470 Mbps to serve all passengers — current LEO systems deliver 100–350 Mbps. The gap is structural, not temporary: adding bandwidth without managing demand does not close it. (Moment IFC Report 2025, modeled from Arcom/Arcep and Viasat data)

- A hybrid IFE architecture reduces satellite bandwidth consumption by 70–90% on narrow-body routes. Embedding content and services locally — and reserving satellite capacity for real-time use — is the only cost-sustainable path to consistent onboard connectivity quality. (Moment IFC Report 2025)

- Hardware costs range from $250,000 to $500,000 per aircraft, with monthly service fees from $500 to over $50,000. ROI depends entirely on whether the airline generates revenue from the connectivity layer — operators without a monetization architecture are paying for infrastructure that funds their ISP, not their P&L. (Moment IFC Report 2025)

- The connected aircraft market will exceed $19 billion by 2033, up from $5.8 billion in 2023. Airlines defining their connectivity architecture now will have a structural cost and experience advantage over those making reactive decisions under passenger pressure. (Novaspace / The Brainy Insights)

- Satellite congestion, regulatory restrictions, and coverage gaps make a single-provider strategy a commercial liability on global route networks. Most airlines operating internationally require multiple ISPs — which makes operator-owned portal governance the critical missing layer. (Moment IFC Report 2025)

The inflight connectivity market is growing. The gap between expectation and delivery is not closing fast enough.

Over 11,000 commercial aircraft were equipped with inflight connectivity by 2024. That number is projected to reach 22,337 by 2033. The connected aircraft market, valued at $5.8 billion in 2023, is expected to exceed $19 billion by 2033 (Novaspace, The Brainy Insights), driven by growing passenger demand for airline Wi-Fi and aircraft connectivity as a standard service.

Passengers today expect the same digital experience in the air as on the ground: HD video streaming, video calls, live TV, messaging. That expectation is not changing. What airlines are navigating is the gap between what passengers want and what current infrastructure can realistically deliver.

This report maps that gap across technology, cost, bandwidth, and architecture, and outlines the strategic approach that closes it.

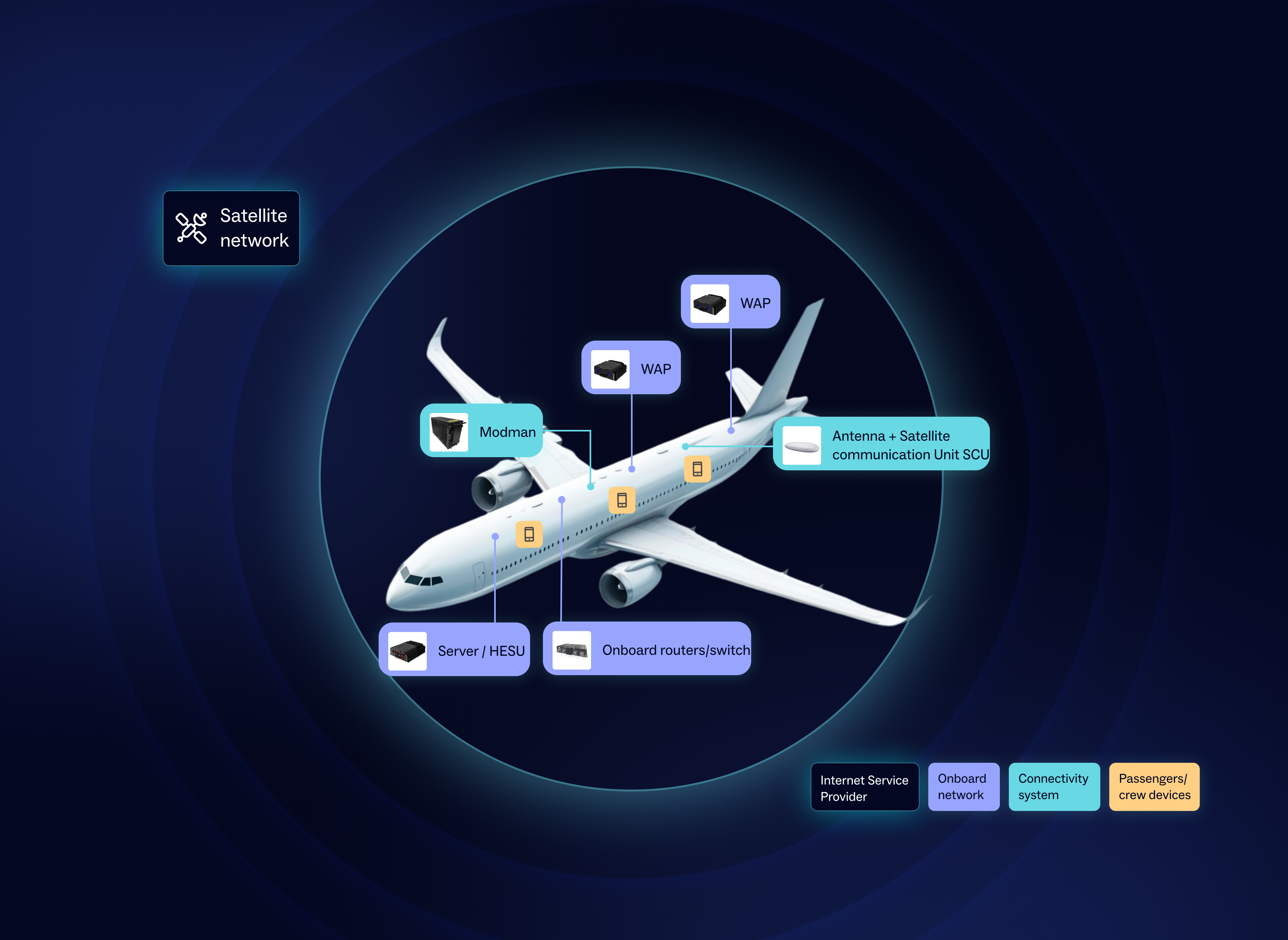

How inflight connectivity works: ATG, LEO and GEO

To enable inflight connectivity, airlines must choose the right infrastructure based on their route network, fleet type, and service goals. Three technologies dominate the market.

ATG (Air-to-Ground) connects aircraft to ground-based towers. Low latency (20-100ms), simpler infrastructure, cost-effective, but limited to regions with dense ground coverage and unavailable over oceans. Bandwidth caps around 20-40 Mbps make it unsuitable for high-density or long-haul routes.

LEO (Low Earth Orbit) satellites, led by Starlink and OneWeb, offer very low latency (20-40ms), global coverage including oceans and poles, and bandwidth ranging from 100-350 Mbps per aircraft. The constraint: satellite tracking requires complex onboard antennas, and availability remains uneven by region and regulatory environment.

GEO (Geostationary) satellites provide broad continental coverage with mature infrastructure. Bandwidth of 70-100 Mbps. The trade-off: high latency (~600ms) and risk of beam congestion on heavily trafficked routes.

Most airlines combine technologies depending on route geography. Ensuring global coverage often requires working with multiple providers, which adds operational complexity and cost.

IFC: a strategic but costly investment

Installing inflight connectivity is not plug-and-play. Hardware costs alone, covering antennas, modems, and onboard network infrastructure, range from $250,000 to $500,000 per aircraft, based on market data from connected aircraft programs. Monthly service fees vary from $500 to over $50,000 depending on bandwidth and data volume.

The ROI depends heavily on airline business model, route structure, and the ability to generate revenue from connectivity through paid access, advertising, or retail. For regional carriers operating narrow-body short-haul routes with thinner margins, the investment calculus looks very different from a long-haul wide-body operator.

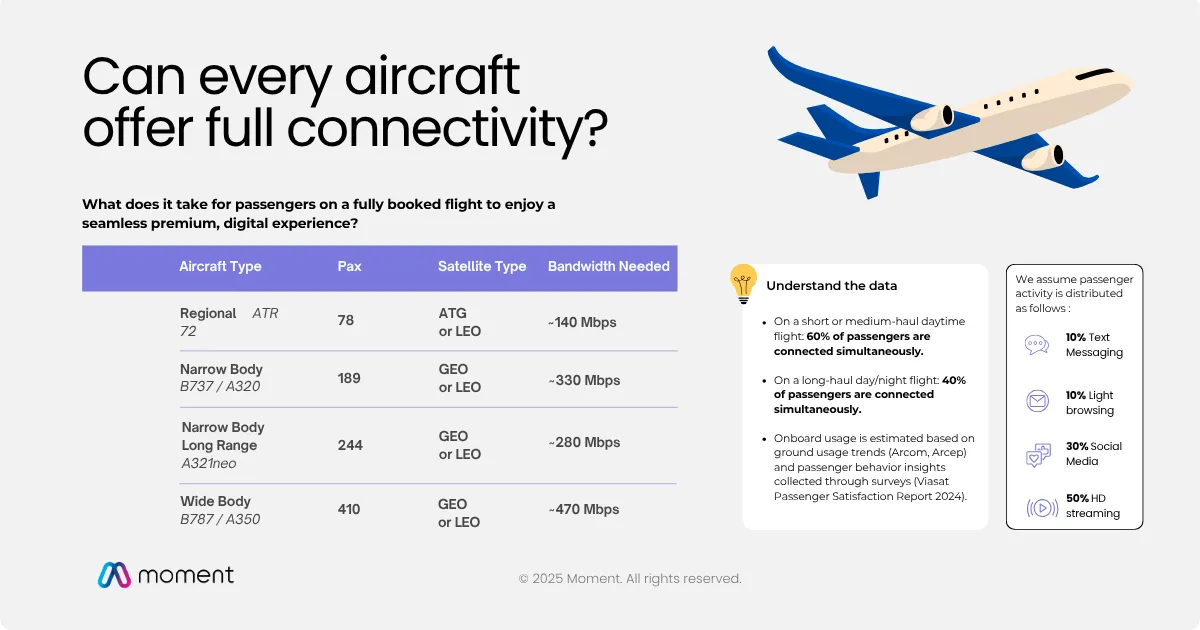

Can every aircraft offer full connectivity?

Bandwidth is a shared resource. On a fully booked flight, even a small number of passengers streaming HD video places significant strain on the system.

Based on realistic usage modeling across passenger behaviors and connection rates (Arcom/Arcep ground usage trends and Viasat Passenger Satisfaction Report 2024), the bandwidth requirements by aircraft type are clear:

A regional ATR72 (78 pax) needs approximately 140 Mbps. A narrow-body B737/A320 (189 pax) needs approximately 330 Mbps. A wide-body B787/A350 (410 pax) needs approximately 470 Mbps.

Even the latest LEO satellite providers promote speeds of 100-350 Mbps per aircraft. A fully connected wide-body long-haul flight requires bandwidth that today's most advanced systems cannot consistently deliver.

This is the operating constraint that defines IFC strategy in 2025. It requires a structural response, not a bandwidth upgrade.

Current limitations in inflight connectivity

Scaling connectivity across global fleets runs into six structural constraints that no single technology has solved.

Bandwidth limits. Most current IFC systems deliver 10-100 Mbps. Even advanced LEO networks struggle to guarantee 1 Gbps dedicated per aircraft when multiple planes operate under the same beam.

Satellite congestion. With over 14,000 commercial flights airborne simultaneously, network saturation is a growing challenge that degrades service quality at peak times.

Coverage gaps. LEO constellations are still in deployment. Long-haul routes such as New York to Hanoi require multiple satellite handovers across providers, adding complexity and cost.

Regulatory restrictions. Satellite internet requires national regulatory authorization in each territory. Coverage availability does not mean service authorization.

Weight. Antennas, modems, and cabling add meaningful hardware weight, which affects fuel consumption, particularly on smaller aircraft where every kilogram counts.

Cybersecurity exposure. Growing connectivity increases attack surface, from passenger data interception to threats reaching onboard systems through poorly secured networks.

The structural response: hybrid IFE and connectivity architecture

The answer emerging across the industry is a hybrid model, combining satellite connectivity with embedded onboard systems to manage bandwidth demand rather than simply adding capacity.

For a hybrid IFE architecture, embedded systems handle locally stored content, food ordering, flight information, and retail. Satellite bandwidth is reserved for real-time services: messaging, browsing, payments, and premium streaming. On a narrow-body short-haul flight, this approach reduces bandwidth consumption by 70-90% compared to a full-cloud model.

The operational benefits are measurable: lower recurring bandwidth costs, more predictable service quality regardless of passenger load, and a branded experience that the airline controls rather than the ISP. A well-configured inflight connectivity strategy starts with this architecture decision. The Wi-Fi portal layer governs access, monetisation, and security across the full architecture.

What this means for airline IFE, engineering and connectivity teams

The connected aircraft market doubles by 2033. Airlines defining their connectivity architecture now will have a structural cost and experience advantage over those making reactive decisions under passenger pressure.

The full report includes bandwidth modeling by aircraft type, cost-per-passenger analysis across fleet configurations, a Starlink pricing benchmark, and a framework for evaluating hybrid IFE and connectivity architectures. Used by IFE managers, CAMO teams and engineering leads at airlines evaluating their inflight connectivity solutions. Free download. Practical, not theoretical.

Frequently asked questions

Why do passengers rate inflight Wi-Fi poorly even when connectivity is available?

Because bandwidth is shared. On a fully booked narrow-body flight, the system needs approximately 330 Mbps to serve all passengers — most IFC systems deliver 10–100 Mbps. The result is degraded speed at peak usage moments, regardless of what the service agreement says about available capacity. Connectivity being "on" and connectivity being usable are two different things. Airlines that manage bandwidth demand — rather than simply buying more capacity — consistently deliver better passenger satisfaction per dollar spent.

What do passengers expect from inflight Wi-Fi in 2025?

Passengers expect the same experience they have on the ground: HD streaming, messaging, and browsing without interruption. Approximately 80% now consider inflight Wi-Fi essential, on par with seat comfort. The critical shift is that expectation is no longer benchmarked against "inflight Wi-Fi" — it is benchmarked against ground 4G/5G. Airlines that cannot meet that bar reliably face measurable NPS impact on connected routes.

What is the most effective architecture for inflight connectivity in 2025?

A hybrid model: embedded systems handle locally stored content, food ordering, retail, and flight information; satellite bandwidth is reserved for real-time services. This approach reduces bandwidth consumption by 70–90% on narrow-body routes compared to a full-cloud model, lowers recurring costs, and delivers a consistent passenger experience regardless of how many passengers are simultaneously connected. It is also ISP-agnostic — the airline controls the experience rather than the provider.

How much does it cost to install inflight connectivity on an aircraft?

Hardware costs alone — antennas, modems, and onboard network infrastructure — range from $250,000 to $500,000 per aircraft. Monthly service fees vary from $500 to over $50,000 depending on bandwidth volume and data plan structure. For regional carriers on short-haul narrow-body routes, the investment calculus is very different from a long-haul wide-body operator: route economics, passenger yield, and the ability to generate ancillary revenue from the connectivity layer determine whether the investment is self-funding.

Discover our latest reports

Ready to redefine your journey with innovative solutions?

Start powering your digital journey with Moment.