Wi-Fi Portal for Airlines and Transport Operators: Monetise and Control Onboard Connectivity

Aviation, rail and maritime operators face the same challenge: connectivity costs are rising, and the Wi-Fi portal is still treated as a login page. This playbook gives you the governance framework to change that. 10 questions to answer before deploying, with a structured approach to access rules, monetisation and fleet-wide performance.

The market is growing. The control problem is not solved.

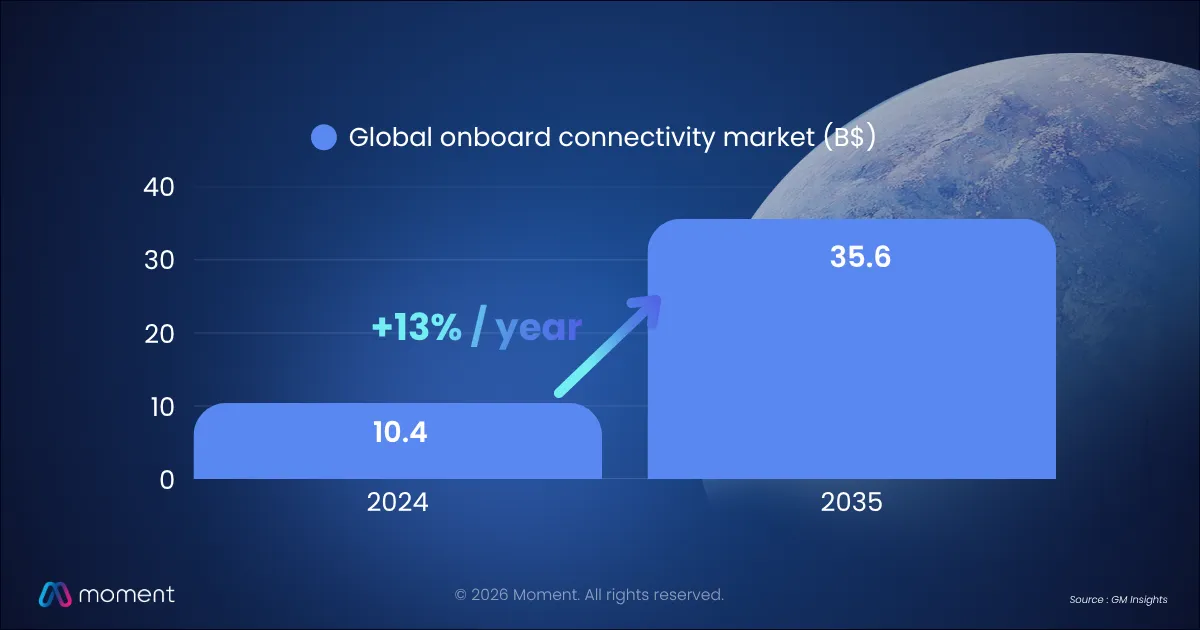

The global onboard connectivity market reached $10.4 billion in 2024. It is projected to exceed $35.6 billion by 2034, with 13% annual growth driven by LEO satellite deployment, 5G integration, and rising passenger expectations across aviation, rail and maritime.

Bandwidth is getting cheaper and more capable. But bandwidth alone does not create value. Control does.

For most operators, connectivity is already a heavy financial commitment: equipment, certification, vehicle downtime, recurring bandwidth costs, adding up to millions per fleet. Yet value generation stalls because the levers that drive adoption and conversion sit with the ISP, not the operator. Access rules, pricing, packaging, A/B testing by route: none of these are in the operator's hands by default.

That is what the Wi-Fi portal changes.

The Wi-Fi portal is not a login page

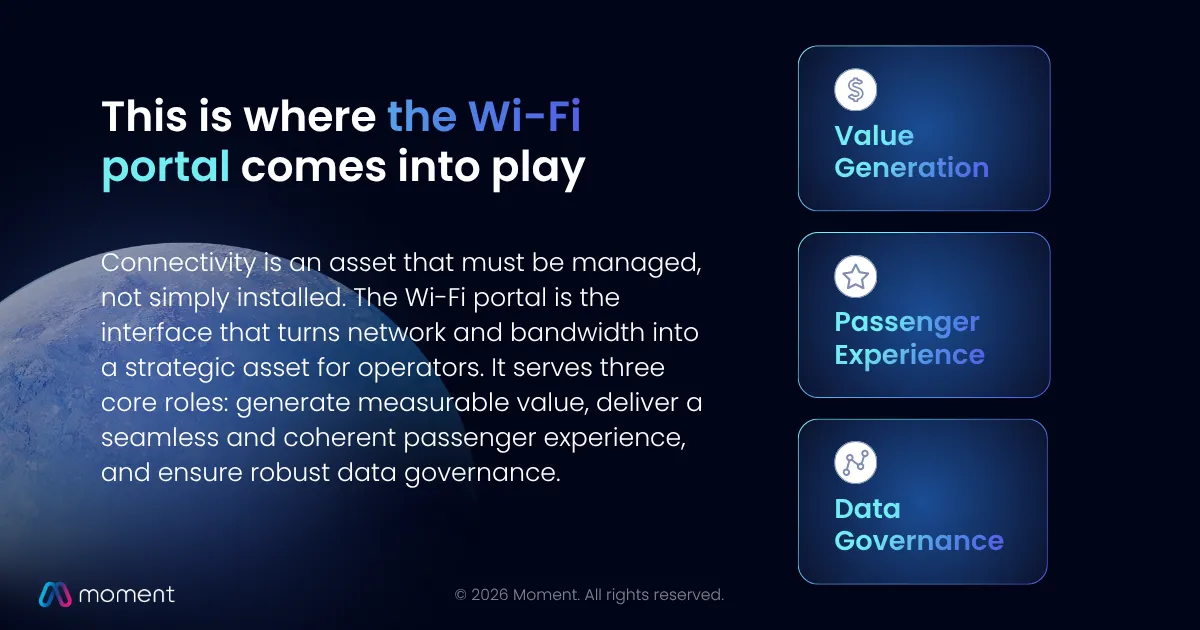

A Wi-Fi portal is the software layer that sits between onboard connectivity infrastructure and passengers. It controls access authentication, offer presentation, payment processing, QoS rules and data collection, independently from the connectivity provider.

It is the operator's control layer between connectivity infrastructure and passengers. Without it, the ISP controls the passenger journey and, by extension, monetisation, data ownership, experience consistency, and ROI.

The portal sits between the network and the passenger. It serves three functions that directly determine commercial performance: value generation, passenger experience, and data governance. Each one depends on who holds the controls.

To deploy and manage that control layer across fleets, Moment's Wi-Fi Portal platform is designed to operate independently from any ISP or connectivity architecture.

How the connectivity challenge differs by transport sector

The infrastructure challenge is largely solved across aviation, rail and maritime. The value generation challenge is not.

Aviation. More than 70% of airlines now offer onboard Wi-Fi. 80% of passengers consider it essential, on par with seat comfort. The market has moved fast: 58% of connected airlines operate freemium models, loyalty-gated access is expanding, and ISP-controlled portals are increasingly a competitive liability. The real challenge is optimising access rules by route, converting connectivity into ancillary revenue, and capturing CRM data that currently flows to the provider. Airlines without an operator-owned portal are paying for bandwidth while the ISP captures the commercial value.

Maritime. Maritime was the first transport sector to deploy satellite connectivity, long before aviation. That early adoption is now a liability for operators who built their model around pay-per-GB pricing. LEO satellite costs dropped 10% in 2024-2025, compressing retail margins while passenger and crew expectations continue to rise. The challenge differs across segments. Ferry operators need to differentiate offers by crossing duration and passenger profile. Cruise operators require multi-language portals with entertainment integration and high-density bandwidth management. Crew welfare deployments on cargo vessels prioritise offline-first access and bandwidth efficiency. Across all three, operators must shift toward differentiated offer models: free, hybrid, sponsored. They need to retain control over pricing and packaging rather than defaulting to provider-driven structures. Without a central onboard connectivity portal, connectivity becomes a commodity across all maritime segments.

Rail. Unlike aviation and maritime, rail still relies primarily on 4G/5G terrestrial infrastructure. Journeys are shorter, but new travel patterns, remote working and extended leisure travel, have turned connectivity into a core quality-of-service requirement. 95% of equipped European rail operators currently offer free Wi-Fi. 89% of rail industry professionals consider connectivity vital for the sector's future. The problem: LEO deployment is now raising CAPEX/OPEX against a free-by-default access model that was never designed for today's cost structure. Rail operators need a control layer that turns connectivity from a cost line into measurable value for the onboard passenger experience.

What operators get wrong without an operator-owned portal

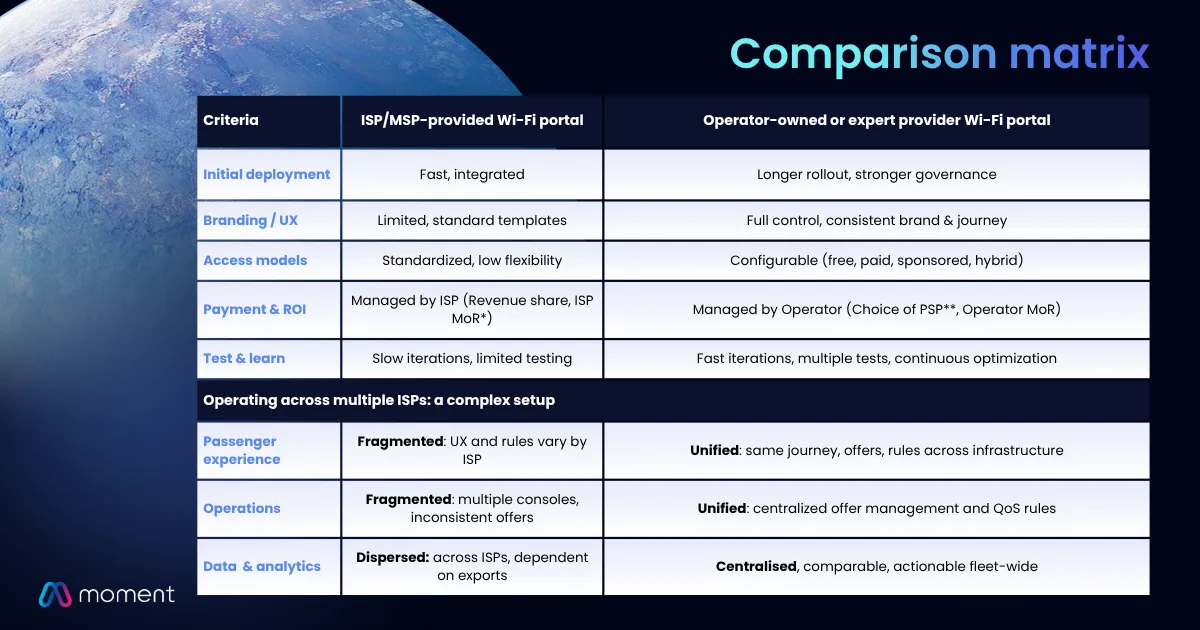

Fragmentation in multi-ISP environments. When multiple connectivity providers serve the same fleet, passengers get different experiences depending on which ISP covers their route. Different UX, different access logic, different rules. Without a central portal, there is no way to unify the journey. The operator pays for multiple infrastructures and delivers a fragmented product.

Revenue left with the provider. ISP-managed portals typically operate on a revenue share model where the ISP acts as merchant of record. The operator receives a portion of what passengers pay but has no visibility into conversion rates, no ability to run pricing tests, and no control over the upgrade logic that drives ARPU.

Data that does not belong to you. Passenger behaviour data, connection patterns, session length, upgrade decisions, drop-off points, is generated on your network, on your vehicles, during your service. In an ISP-managed model, that data sits in the provider's infrastructure. Exporting it requires negotiation. Acting on it in real time is rarely possible.

5 questions to ask before implementing a Wi-Fi portal

These are the questions that determine whether an operator controls its connectivity strategy or depends on its ISP for every adjustment.

1. Do you control access rules independently from your ISP?

Offers, pricing, A/B testing by route and passenger profile, or does every change require a provider ticket and a waiting period?

2. Can you deliver a consistent experience across multiple ISPs?

Or does your fleet fragment by provider: different UX, different rules, different data silos for each connectivity contract?

3. Do you own your payment flows?

PSP choice, 3DS2/SCA compliance logic, refund rules, fraud prevention, or does the ISP act as merchant of record and take a cut of every transaction?

4. Who owns the data generated onboard?

Can you access and export behavioural, commercial and network data in real time, or does it sit in the provider's infrastructure, available only on their terms?

5. If you change ISP or connectivity architecture, do you keep your portal?

Contractual independence from your connectivity provider determines your long-term strategic flexibility and your ability to negotiate.

The full playbook covers 10 questions operators should answer before rolling out a portal, and what the wrong answers cost in terms of margin, data, and operational control. It includes a detailed comparison of ISP-provided vs operator-owned portal architectures, sector-specific configurations, and the compliance requirements that apply across aviation, maritime and rail environments. For operators defining their broader inflight connectivity strategy, the playbook sits alongside the infrastructure decisions.

The playbook is used by IFE managers and connectivity leads at airlines, rail operators and maritime companies to evaluate portal vendors and structure RFPs. 15 pages. Practical, not theoretical.

Questions operators ask about Wi-Fi portal deployment

What does a Wi-Fi portal integrate with onboard?

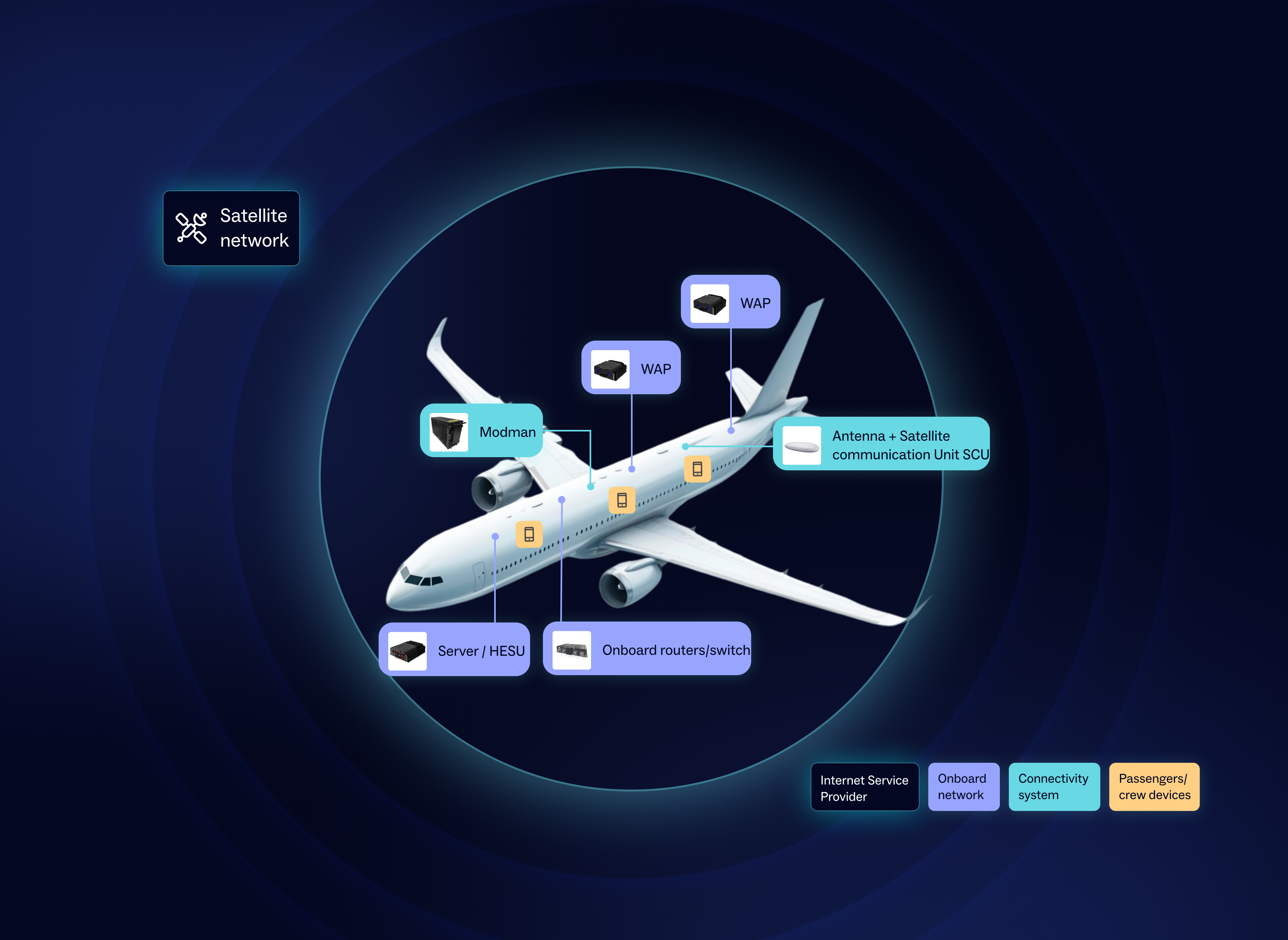

The portal integrates via API with the ISP network layer for bandwidth awareness and session control, with PSPs for payment processing, and optionally with PMS, CRM and loyalty systems for passenger recognition. It runs as a lightweight VM or container within existing onboard IFEC infrastructure, with no hardware overhaul required.

How long does it take to deploy an operator-owned Wi-Fi portal?

Deployment timelines depend on integration scope. A cloud-based configuration with a Moment-certified PSP and no CRM integration can go live faster than a full enterprise deployment with loyalty and multi-ISP management. Integrations are deployed progressively: not all are required on day one.

Does an operator-owned portal work across aviation, rail and maritime?

Yes. The same portal architecture applies across transport modes, with sector-specific configurations: offline-first mode for maritime crew welfare deployments, route-based QoS rules for rail, and cabin class segmentation for aviation. The compliance layer adapts to the regulatory requirements of each environment.

Discover our latest reports

Ready to redefine your journey with innovative solutions?

Start powering your digital journey with Moment.